Authors:

Lew Daly, Just Solutions

Doug Koplow, Earth Track

Key Report Findings

The 45Q tax credit expansion for Carbon Capture, Utilization, and Storage, passed as part of the Inflation Reduction Act of 2022, dramatically increases the expected cost to taxpayers without adequate oversight or transparency to ensure fiscal integrity or program efficacy. Independent analyses suggest tax subsidies could average $46 billion per year—more than 140 times the original official projections. Total costs could reach as high as $835 billion by 2042; and were industry-proposed expansions implemented, the taxpayer cost could surge above $2 trillion. With lax oversight, little transparency, and most credits funding enhanced oil recovery rather than true carbon reduction, the risks to taxpayers are enormous. This report examines the 45Q program’s potential fiscal impacts and the urgent need for reform of this flawed federal subsidy.

TAXPAYER COSTS FOR CARBON CAPTURE, UTILIZATION, AND STORAGE: A Fiscal Disaster in the Making

Expanded CCUS Tax Credits Means Much Higher Costs for Taxpayers

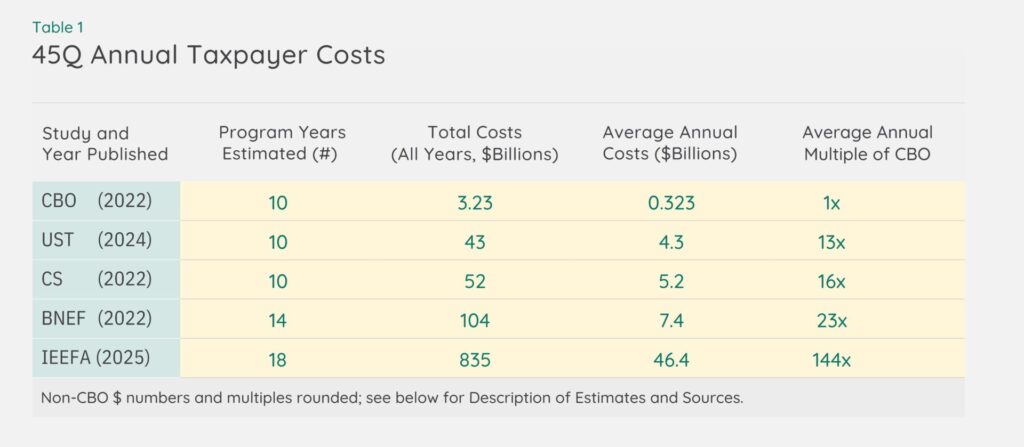

The Inflation Reduction Act (IRA) greatly expanded the 45Q tax credit program for Carbon Capture, Utilization, and Storage (CCUS).1 The breadth of eligible claimants is now much broader and the monetary value of credits larger across all eligible types of CCUS projects. In addition, the timeline of credit availability is now significantly extended, with new projects able to be placed in service under 45Q until 2032 rather than the end of 2025 under prior law. With a 12-year eligibility period, credits are available well into the 2040s. Taken together, these policy changes raise serious concerns for taxpayers about skyrocketing program costs. Independent analyses of the potential taxpayer costs of 45Q are strikingly higher than federal estimates, underscoring the potential scale of fiscal impacts and the need for much greater tracking and control of the subsidy. One leading independent analysis, based on actual CCUS projects under development, estimates that 45Q costs will average about $46 billion annually between 2025 and 2042.2 This is more than 140 times larger than the original 45Q “score” in Congressional Budget Office (CBO) analysis of the Inflation Reduction Act as enacted, which projects average annual costs of approximately $323 million over a decade.3 In Table 1, we summarize average annual costs of 45Q as estimated in both government and independent analyses. Although the average annual values clearly reflect significant discrepancies between government and independent estimates, Table 1 also includes data on the number of years covered and total projected costs, elements with significant implications for taxpayers that are discussed in more detail below.

Such large gaps between estimates may seem anomalous; however, the outlier in this comparison is not the much higher independent estimate (IEEFA) but rather the much lower initial government estimate. Based on the available 45Q credit value of actual CCUS projects currently in the development pipeline, the independent upper-end estimate provides a more realistic outlook for taxpayer costs.4 By comparison, government estimates (the full details of which are not made public) primarily extrapolate from historical budget trends, adjusting for policy changes and incorporating only limited information about commercial activities and potential market growth. Further, CBO estimates of tax legislation are limited to a 10-year “post-legislation” window (in this case, 2022-2031), which truncates the scoring timeframe to less than half of the total timeline for 45Q credit availability under current law. Treasury reports also have a 10-year window. As a result, the federal estimates effectively “miss” much of the likely growth in 45Q costs, which will accrue throughout the 2030s from currently announced and new projects being placed in service over the next several years prior to the 2032 deadline for accessing credits. This timing gap between federal estimates and the 45Q program is a major reason why the IEEFA estimates are so much higher, along with the use of more robust and current data on CCUS project pipelines. With that said, a more recent government estimate by the Department of Treasury, likely reflecting newer market assessments than were available in the pre-IRA period, indicates annual 45Q spending at an average rate of $4.3 billion over a decade. This is significantly higher than the original CBO score, though still more than ten times lower than estimates based on current commercial information and legislated program timelines.

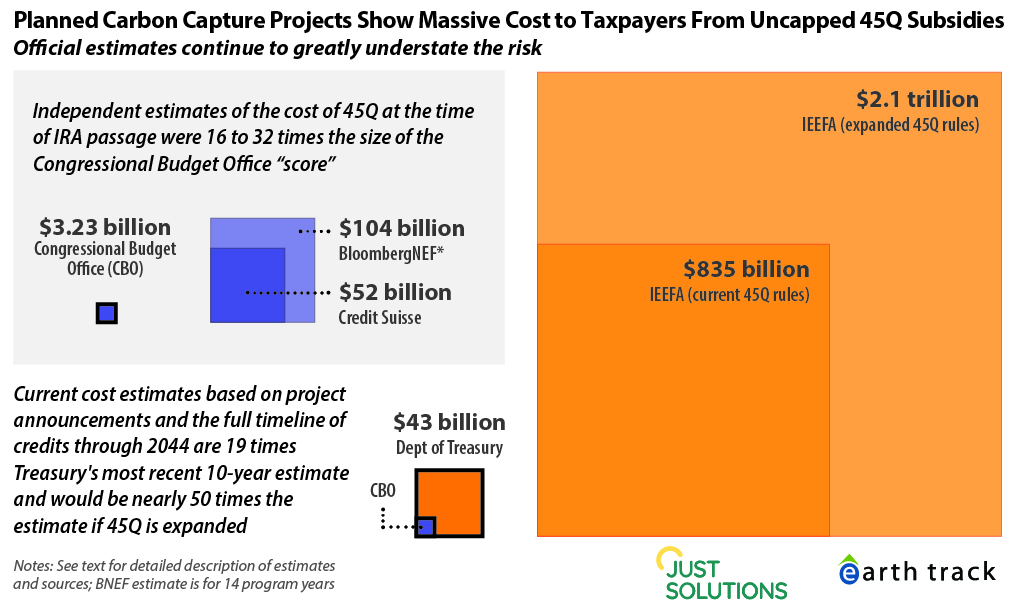

Overall, multiple independent estimates based on current law consistently indicate much higher costs than originally projected. Estimates done concurrently with passage of the IRA by Credit Suisse and Bloomberg New Energy Finance (BNEF) projected annual average costs between 16 and 23 times higher than the government estimate. As industry assessed the opportunity from increased 45Q subsidies under the IRA, new projects entered the pipeline, and subsequent estimates are more than 140 times higher than the original CBO score. At a minimum, these huge discrepancies in the fiscal impact of 45Q indicate a high level of associated risk to taxpayers. The truly alarming implications, however, become much clearer in considering the cumulative scale of 45Q spending across the current—and potentially extended—timeframe of the program.

As seen in Figure 1, with the current window of credit availability remaining open until 2044, the cumulative fiscal price tag of 45Q is potentially staggering: as much as $850 billion by 2042 and rising to more than $2 trillion if credit values were further enhanced and the current 12-year limit for obtaining credits were to be extended. Extension seems likely, as high operating costs could lead to project terminations if subsidies cease, which runs counter to the carbon dioxide (CO2 )-reduction goals of 45Q.5 Moreover, this estimate is based on a CCUS project pipeline as of early 2025; since 45Q has no cap, taxpayer costs will almost certainly rise in the likely event that new projects “pile into” the queue as the 2032 eligibility deadline approaches. Finally, industry proposals have already created a policy road map for expanding CCUS, including detailed proposals for enhancing the 45Q program in the future.6 As noted above, the 45Q enhancement scenario illustrated in Figure 1 would result in more than doubling the cost of the program as estimated under current law.

45Q Program Flaws Amplify Concerns about Fiscal Waste

- Poor targeting for uncertain climate benefits. The limited available data on claimants indicate that the vast majority of 45Q credits support enhanced oil recovery (EOR) operations. Because credit amounts are based on gross tons of CO2 sequestered, as opposed to net CO2 reductions that deduct the additional CO2 emissions from combustion of the recovered oil, these credits may result in subsidizing additional carbon pollution, contrary to legislative intent.7 The considerable uncertainty of climate benefits of an EOR-heavy 45Q footprint in the economy sharply underscores the potentially disastrous fiscal impacts of 45Q.

- Inadequate oversight. Existing oversight related to CCUS is delegated to the U.S. Environmental Protection Agency (EPA) and the U.S. Department of the Treasury. EPA receives self-reported sequestration data from facilities, which is not verified by the Agency.8 At the same time, Treasury does not report 45Q credit claims except in the form of aggregate tax expenditures and thus it is impossible to publicly track credit claims against the (itself unverified) EPA data on sequestration amounts.9 Taxpayers have no assurance that 45Q is delivering CO2 reductions in line with fiscal costs of the program.

- No fiscal transparency. From a more general standpoint of fiscal integrity, information about credit claimants and credit amounts is shielded from disclosure by tax information confidentiality rules, except in very limited circumstances such as criminal investigations.10 The allowable types of disclosure do not include the public interest in transparency of corporate tax subsidies. The public essentially has no direct, project-specific information to assess the costs of credits and to identify the corporations and activities being supported by federal tax dollars.

Taxpayers Need Protective IRS Reforms for Transparency and Public Disclosure of 45Q Credit Information

- Guardrails on credit amounts. This could include setting a cap on the total amount of credits that can be claimed in a given period, following the approach used in other tax credit programs such as Internal Revenue Code Section 48C for Qualifying Advanced Energy Projects.11

- Transparency and accountability requirements. Specific requirements to ensure greater transparency of tax credit information are also important, including public disclosure of tax credit amounts allocated to 45Q claimants, detailed information about credited projects and credit transfer activities, as well as more stringent criteria for auditing, recapture of credits, and other factors for accountability of programmatic implementation and results.

Description of Estimates and Sources

Official Estimates

CBO: Congressional Budget Office “score” of the cumulative budget impact of the 45Q credit program as amended by the Inflation Reduction Act, at $3.23 billion in revenue losses for the period of 2022-2031. The CBO score is divided between $1.68 billion in revenue losses and $1.55 billion in “outlays,” referring to direct credit payments claimed under the IRA’s “elective pay” provision. Eligible entities for elective pay are normally tax-exempt organizations, such as governmental bodies or cooperatives; however, 45Q also allows this option for some taxable corporations as well, on a limited basis. Source: Congressional Budget Office, “Estimated Budgetary Effects of Title I, Committee of Finance, of Public Law 117-169, to Provide for Reconciliation Pursuant to Title II of S. Con. Res. 14,” September 7, 2022.

UST: United States Treasury estimate of 45Q tax expenditures at $43.4 billion between 2025-2034. This measure includes estimated credit expenditures at $25.21 billion as well as $18.2 billion in “outlay tax expenditures” (elective pay credits). Source: U.S. Department of the Treasury, Office of Tax Analysis, Tax Expenditure Budget for Fiscal Year 2026, Tables 1 and 5, November 27, 2024.

Independent Estimates

CS: Credit Suisse estimate of 45Q costs at $52 billion for the period 2022-2031. The report identifies 45Q as having the “largest spending delta” between its spending estimate and the official estimate, driven by much higher expected point source CO2 capture—100 million tons per annum as of 2030 as compared to approximately 4 million tons by 2030 in the CBO estimate. Source: Credit Suisse, “US Inflation Reduction Act–A tipping point in climate action,” 2022.

BNEF: Bloomberg New Energy Finance estimate of 45Q costs at $104 billion for the period 2024-2037. The estimate is based on announced CCUS projects as of 2021, assuming 12 years of eligibility and no extension. Their method is comparable to the IEEFA estimates (below) but relies on older project data, prior to a large shift in project development over the last two years partly in response to enhanced 45Q credits. The BNEF report does note that their estimate is likely conservative because of new projects that will be put into service closer to the 2032 eligibility deadline. Source: Julia Attwood, “Carbon Capture Could Get $100B in Credits from US Climate Bill,” Bloomberg NEF, August 16, 2022, subscription only.

IEEFA: Institute for Energy Economics and Financial Analysis estimate of 45Q costs at $835 billion for the period 2025-2042. This estimate is based on CO2 capture estimates of 142 announced projects in the Clean Air Task Force (CATF) project database as of January 2025. This comprises just under two-thirds of the total projects listed by CATF. The second IEEFA estimate of $2.1 trillion is for the same set of projects, but accounts for policy changes that increase the credit amount and extend eligibility to 30 years. Source: Institute for Energy Economics and Financial Analysis, Tax credits for carbon capture utilization and storage, February 11, 2025.

Endnotes

1 Congressional Research Service, “The Section 45Q Credit for Carbon Sequestration,” August 25, 2023.

2 Institute for Energy Economics and Financial Analysis, Tax credits for carbon capture utilization and storage, February 11, 2025. We calculate the annual average based on the cumulative estimate of $835 billion over 18 years.

3 Congressional Budget Office, “Estimated Budgetary Effects of Title I, Committee of Finance, of Public Law 117-169, to Provide for Reconciliation Pursuant to Title II of S. Con. Res. 14,” September 7, 2022. For comparison, we calculate the annual average based on the CBO score of $3.23 billion over 10 years.

4 For the data on current projects in development, see Clean Air Task Force, U.S. Carbon Capture Activity Project Table. CATF data accessed by IEEFA in January 2025.

5 Pat Knight and Jack Smith, “Clearing the Air on Coal CCS: New tax credits make partial CO2 capture viable, potentially increasing emissions,” Synapse Energy Economics, October 21, 2022. See also Emily Grubert and Frances Sawyer, “US power sector carbon capture and storage under the Inflation Reduction Act could be costly with limited or negative abatement potential,” Environmental Research: Infrastructure and Sustainability,” Vol. 3, Issue 1 (2023).

6 In 2019, the National Petroleum Council (NPC) issued a comprehensive policy road map for CCUS expansion. Among other recommendations (some of which were subsequently adopted in the IRA), the NPC recommends extending the timeline of credit availability from 12 to 20 years and generally increasing federal f inancial support to $110 per ton. See National Petroleum Council, “Meeting the Dual Challenge: A Road Map to At-Scale Deployment of Carbon Capture, Use, and Storage,” Chapter 3 (updated March 12, 2021). ExxonMobil has engaged in extensive lobbying to enhance the 45Q program in recent years, including proposals to raise the non-EOR 45Q credit value to $100, extend the credit access timeline from 12 to 30 years, and remove the project start deadline (effectively making the credit permanent). See Erik Oswald, Exxon Mobil Low Carbon Solutions, “Advancements in CCS and Hydrogen,” presentation at the Annual Meeting of the Interstate Oil and Gas Compact Commission, November 9, 2021, slide 10. See also Andy Rowell and Nina Lakhani, “How Exxon chases billions in US subsidies for a ‘climate solution’ that helps it drill more oil,” The Guardian, August 29, 2024. The carbon capture industry has also advocated to boost the credits indirectly through modification of an IRA provision to inflation-adjust 45Q credit values starting immediately instead of in 2027, and using 2022 prices as the base year for the adjustment (increasing base values by nearly 15%). See Carbon Capture Coalition, “Federal-Section-45Q-Inflation-Adjustment_FactSheet,” May 2024.

7 Taxpayers for Common Sense, “Hot Air and High Costs: The Carbon Capture and Sequestration Credit,” February 2023, p. 4. This pattern applies globally, and net of incremental fuel extracted and burned, CCUS for EOR often increases CO2 emissions. See Mark Z. Jacobson, et. al.,“Energy, Health, and Climate Costs of Carbon-Capture and Direct-Air-Capture versus 100%-Wind-Water-Solar Climate Policies in 149 Countries,” Environmental Science & Technology, Vol. 59, Issue 6 (2025): 3034-3045

8 In addition to lack of independent verification, EPA requirements for monitoring of, and reporting on, CCUS storage operations are largely left to the discretion of project owners/operators, which is concerning not only from a climate perspective but also from a fiscal perspective given 45Q’s statutory purpose as a production tax credit for carbon sequestration. See Environmental Integrity Project, “Flaws in EPA’s Monitoring and Verification of Carbon Capture Projects,” December 13, 2023.

9 Minho Kim, “Critics Fear Tax Subsidies for Carbon Capture Won’t Be Checked,” The New York Times, September 20, 2024. In response to a Freedom of Information Act request, EPA noted that information on carbon capture tax credit claims did not involve EPA records, and that a search for records related to enforcement of monitoring, reporting, and verification plans (required by EPA to ensure proper CO2 management by firms claiming 45Q credits) came back with nothing. Sharon Lie, Director, U.S. EPA Climate Change Division, Response to Ann Brown, Center for Biological Diversity, July 11, 2024.

10 The Tax Law Center at NYU Law, “Understanding Taxpayer Privacy Protections Under Section 6103 and Related Statutes,” February 10, 2025.